15 Feb, 2023

What does a startup CFO do? – And what are a startup’s CFO’s responsibilities?

Lack financial and other relevant skills required to run a startup or spin-off successfully. Lack of skill set results in…

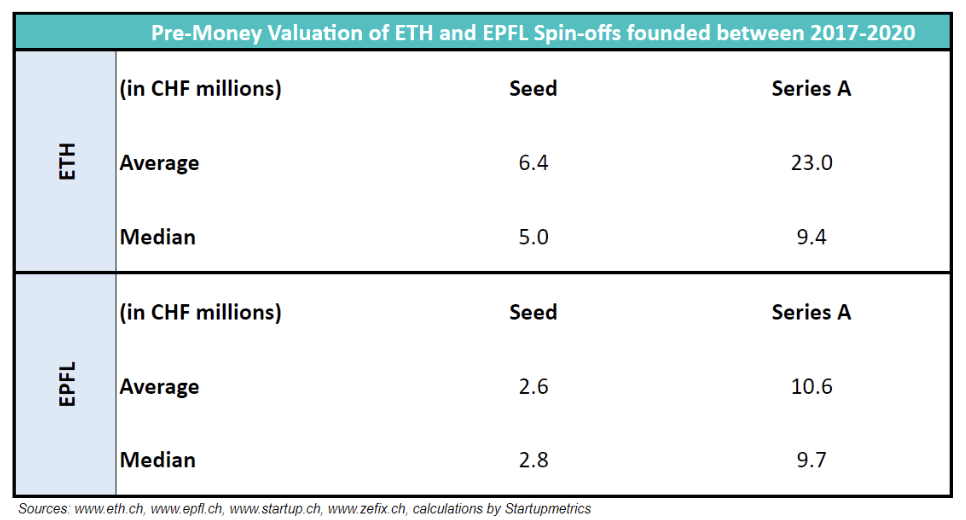

The valuation of pre-revenue start-ups requires a specific data set with comparable transactions. Differences in qualitative factors such as team strength and market potential justify a deviation from the mean. In this post, we briefly discuss the average and median pre-money valuation of early-stage spin-offs from the two top Swiss universities, ETH and EPFL.

The average pre-money valuation in the seed phase is CHF 6.4 million and CHF 2.6 million for ETH and EPFL spin-offs, respectively. The corresponding median value is 5 million CHF and 2.8 million CHF. Thus, the pre-money valuation of an ETH spin-off in the seed stage is likely to be 78% to 146% higher than that of an EPFL spin-off. Moreover, the distribution is skewed to the right. This means that the majority of spin-offs are valued below their average.

The average pre-money valuation of the Series A spin-offs also differs significantly. On average, the pre-money valuation of ETH spin-offs is 116% higher at CHF 23 million compared to CHF 10.6 million. However, the median pre-money valuation of the Series A spin-offs of the two universities is comparable with a deviation of only 3.39%.

Lack financial and other relevant skills required to run a startup or spin-off successfully. Lack of skill set results in…

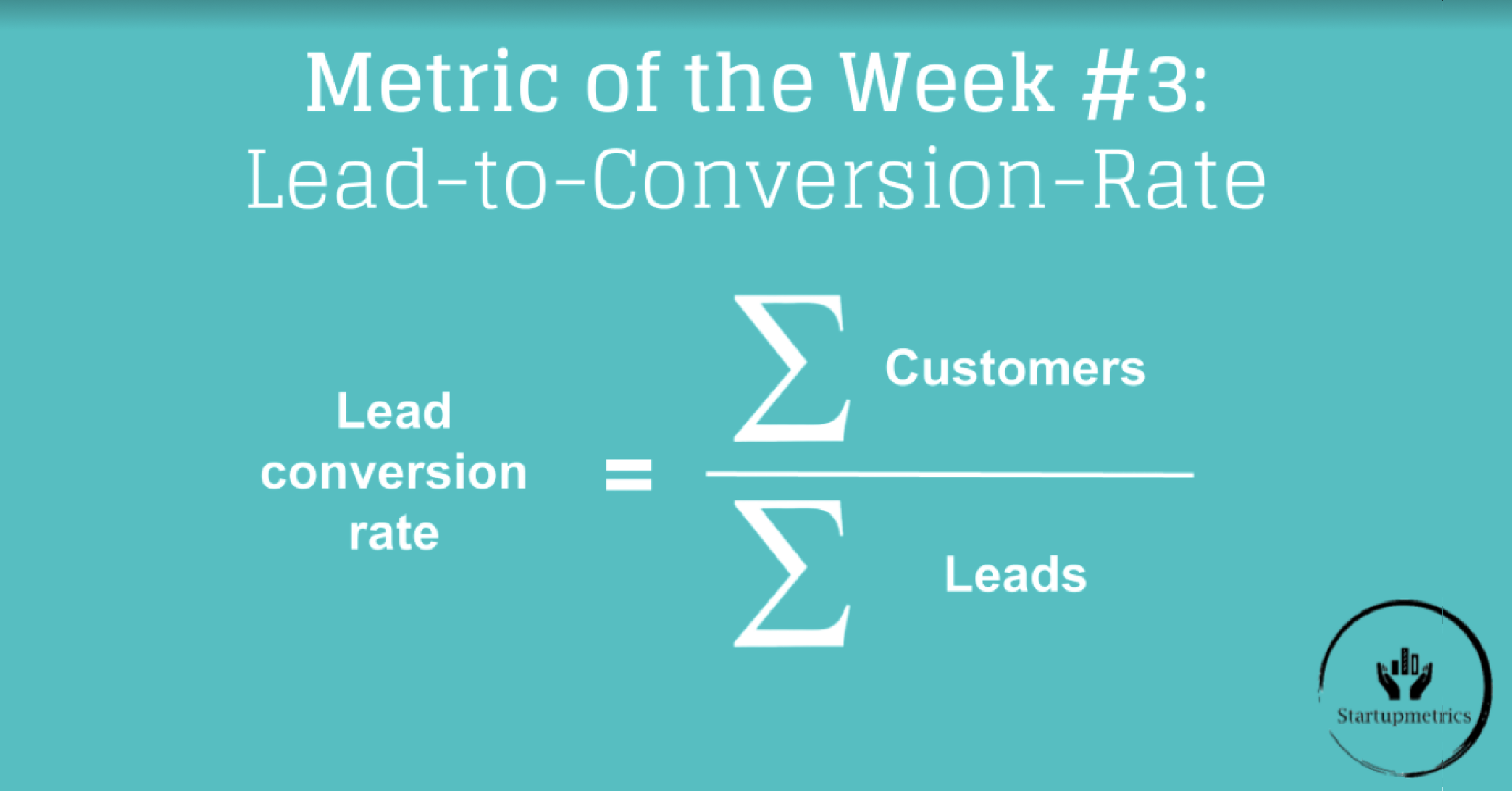

The lead to conversion rate is a valuable metric that tells you how many potential customers you need to connect…

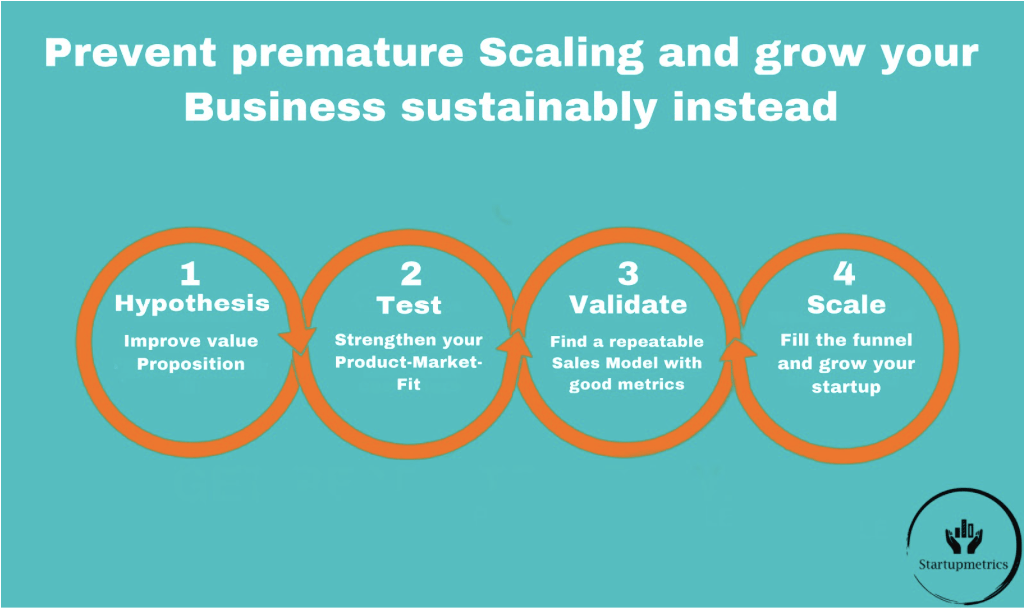

Many business articles list the top reasons why startups fail. However, the biggest cause is usually overlooked, namely premature scaling….

In 2024, the role of the startup CFO extends far beyond traditional financial management. Today’s CFOs are pivotal in strategic…